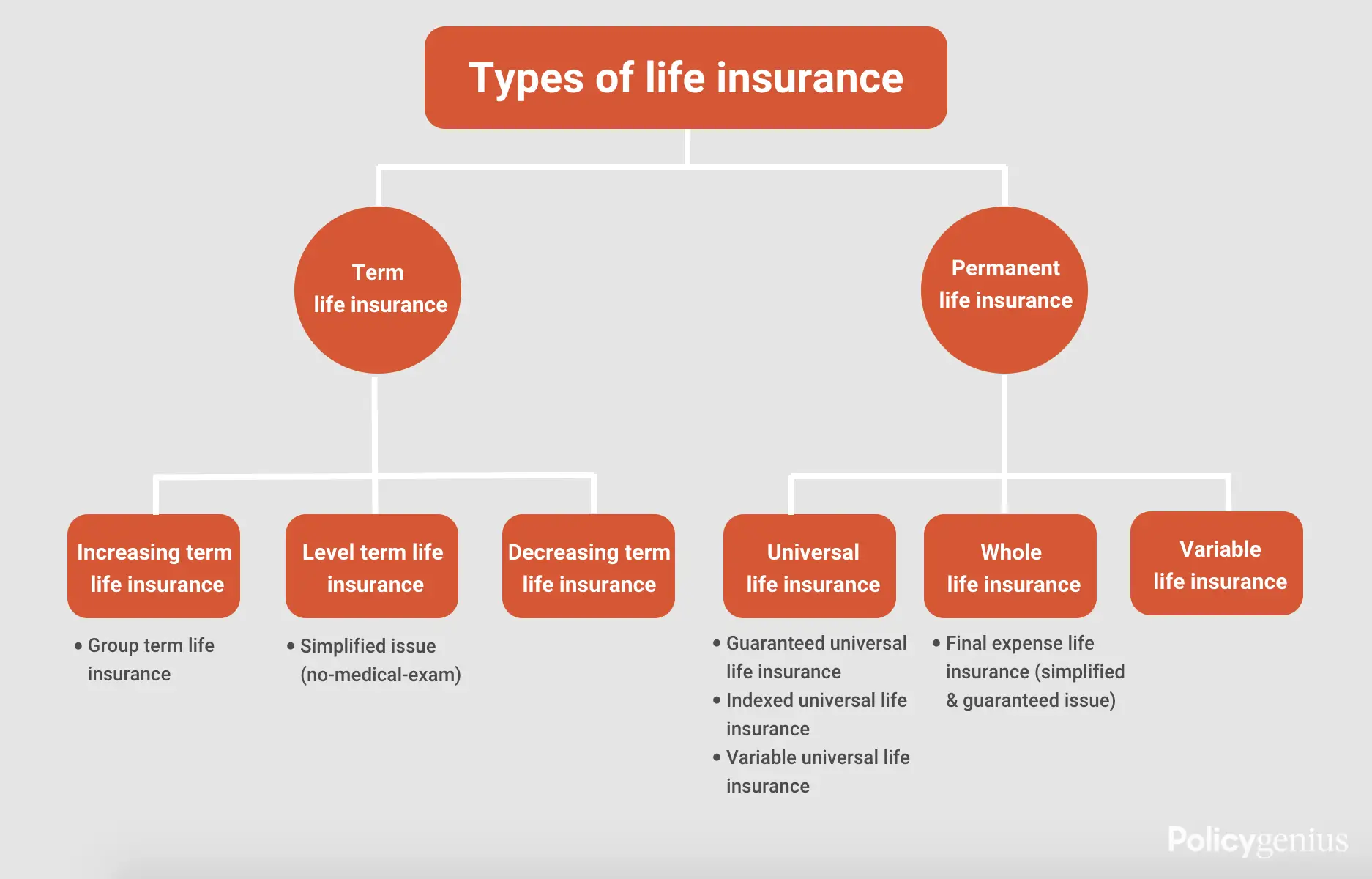

Which Policy Provides the Most Coverage at the Lowest Cost for a Young Family?

Shopping for life insurance can seem overwhelming, but deciding which type of policy you need is simple. There are only ii main policy categories to choose from: term life insurance and permanent life insurance. Term life insurance (the well-nigh popular type of life insurance) lasts for a specific amount of fourth dimension, while whole life insurance (the most popular type of permanent coverage) lasts your unabridged life.

Once you decide between term and permanent coverage, you're already halfway to the finish line. We'll explicate the differences between the two, as well every bit the options within term and permanent life insurance bachelor and so you can cull the 1 that suits you lot best.

Key Takeaways

-

Term life insurance is the simplest and most affordable selection for about people.

-

Whole, universal, and final expense life insurance are all types of permanent life insurance.

-

Some types of permanent life insurance come with a cash value corporeality that works similar an investment account.

-

Some types of life insurance policies are categorized based on medical underwriting or the lack thereof, such as guaranteed upshot life insurance.

Term life insurance

Term life insurance lasts for a set number of years before it expires. Yous pay premiums toward the policy, and if you die during the term, a gear up amount of money, known as the death benefit, is paid to your designated beneficiary . The decease do good can be paid out every bit a lump sum, a monthly payment, or an annuity. About people elect to receive their expiry benefit as a lump sum to avoid taxes.

-

Benefit: affordability Term life insurance policies are less expensive than other types of life insurance policies and mostly take lower premium costs.

-

Downside: length Term life insurance has an expiration appointment, which can marshal with a mortgage or when your children graduate higher. Those looking for lifelong coverage should opt for permanent life insurance instead.

-

Who it's for: almost life insurance shoppers Those looking for cheaper life insurance for up to 30 years should buy term life insurance.

→ Acquire more than about term life insurance

Whole life insurance

Whole life insurance is the well-nigh popular type of permanent life insurance. It also pays out a decease benefit, just unlike term life, almost policies have a cash value, an investment-similar, tax-deferred savings account, included in the policy.

-

Benefit: cash value & lifelong coverage The greenbacks value component tin can comprehend endowments or estate plans. And since this coverage lasts for your entire life, information technology can help support long-term dependents such as children with disabilities.

-

Downside: cost & complication A whole life insurance policy can cost 5 to xv times as much as a term life policy for the same decease benefit amount, based on Policygenius data in January 2022. The cash value component makes whole life more circuitous than term life because of fees, taxes, involvement, and other stipulations.

-

Who it's for: younger buyers who can pay more People who anticipate lifelong dependents or a need for permanent insurance with minimal complexities can benefit from whole life.

→ Acquire more than about whole life insurance

Universal life insurance

There are three types of universal life insurance (UL): indexed universal life insurance (IUL), guaranteed universal life insurance (GUL), and variable universal life insurance (VUL). All have a cash value, just like a whole life insurance policy. Your premiums get toward both the cash value and the decease do good.

Unlike whole life insurance, universal life insurance allows you to subtract (or increment) how much you pay towards premiums (flexible premiums) and allows for adjustable death benefits. If you decrease how much you spend on premiums, the difference is withdrawn from your policy'due south greenbacks value.

Indexed universal life insurance

Indexed universal life insurance is the near popular type of UL. The cash value account has a minimum (and maximum) guaranteed interest rate based on a stock market index (like the S&P 500), chosen by the insurer.

- Do good: cash value gains

There's a potential to see bigger gains in the cash value business relationship compared to other permanent life insurance policies, depending on stock market place performance. - Downside: investment caps

Almost insurers fix limits on greenbacks value gains. Y'all won't lose your base cash value, but dedicated investment accounts will offer higher returns. - Who it'due south for: portfolio enhancers

If you've maxed out other investment accounts or are looking for a relatively safe investment with guaranteed minimum values IUL might be right for yous.

Guaranteed universal life insurance

Guaranteed universal life insurance is universal life insurance without the market risk. Your premiums stay the same regardless of how marketplace indexes perform, as your plan's interest rates are baked into the premiums when y'all sign up for the policy. This type of life insurance has a "no-lapse" guarantee, meaning that as long as you pay your premiums, you'll have coverage.

- Benefit: stability

Guaranteed universal life insurance provides lifelong coverage without the market fluctuations of indexed or variable policies. - Downside: no greenbacks guarantee

Unlike some permanent life insurance, GUL doesn't allow for premium payments from the cash value business relationship. If y'all skip a premium payment, your policy will lapse. - Who it'south for: run a risk-averse people with permanent insurance needs

Guaranteed universal life insurance is a relatively affordable permanent pick, sort of like a term life insurance policy where the term lasts the rest of your life.

Variable universal life insurance

Variable universal life insurance has a variable interest rate set by the life insurance company. Greenbacks value is invested in common funds that tin increase or decrease. It shares elements from universal and variable life insurance policies.

- Benefit: cash value gains

At that place's a potential to see bigger gains in the cash value account compared to other permanent life insurance policies, depending on your investment choices. - Downside: too easily-on

The policyholder, not the insurance company, manages the investment portfolio. Different other types of permanent insurance, you'll need to manage your own greenbacks value investments or work with a separate fiscal counselor. - Who it's for: DIY investors

At that place'due south a big potential upside for policyholders who don't mind being involved in money management.

→ Learn more well-nigh universal life insurance

Variable life insurance

The money paid into a variable life insurance cash value goes into a serial of mutual fund-similar sub-accounts where you can get some decent growth, but y'all can also lose money depending on the market. This blazon of policy's cash value is more than akin to investing.

While this makes variable life insurance policies a better investment option than whole life insurance policies — with potential for higher, tax-deferred growth — you tin only invest in the sub-accounts bachelor through your policy. All of this makes a variable life insurance policy both a limited investment option and a limited coverage choice.

-

Benefit: savings potential Like to variable universal life insurance, policyholders tin can encounter greater cash value gains with this blazon of policy over other permanent products.

-

Downside: high run a risk for policy lapse Both the cash value and expiry benefits can fluctuate based on your portfolio'due south performance.

-

Who it's for: easily-on investors who don't mind hazard For those who desire to take control of their own investment portfolio, in that location's potential for cash gains.

→ Learn more about variable life insurance

Final expense insurance

There are 2 types of final expense life insurance, which fall under the whole life insurance category: simplified issue life insurance and guaranteed upshot life insurance.

Simplified issue life insurance

Simplified issue life insurance allows you to fill out a health questionnaire and skip the medical exam. This is too known as a blazon of no-medical-exam policy.

- Benefit: burying costs

This type of insurance covers the cost of anything associated with your decease, including medical intendance, a funeral, or cremation. It'due south useful if yous don't have another way to pay for your funeral and don't want to burden your family unit with the costs. - Downside: price & health limitations

If you're over a certain historic period, have astringent underlying medical weather condition, are unable to independently fill up out the application, or are a smoker, you may not qualify for simplified consequence life insurance. - Who it'south for: seniors without major medical issues

Information technology'south as well a adept option for adult children looking to purchase life insurance for their aging parents to cover terminal expenses.

Guaranteed issue life insurance

Guaranteed issue life insurance skips both the medical exam and the health questionnaire. As long as you tin can pay the premiums and fill out the awarding with info near your age, sex, and residency, the insurer volition cover you. If an applicant cannot respond questions on the application due to avant-garde dementia or Alzheimer's, then they would not authorize for guaranteed consequence life insurance.

- Benefit: burial costs

Guaranteed issue offers similar benefits to simplified issue policies. - Downside: price

Like other types of final expense life insurance, these policies have higher premiums for relatively depression coverage amounts (typically up to $l,000). - Who information technology's for: seniors or people with terminal illnesses

For older people or those with declining health, guaranteed event life insurance might exist the only option bachelor.

→ Learn more nearly terminal expense life insurance

Group life insurance policies

Group life insurance is an employee benefit provided by some employers that is a blazon of term life insurance called almanac renewable term. It isn't technically a type of life insurance, but it'south of import to know how information technology's different from privately purchased life insurance.

Most people recall their employer-sponsored life insurance is enough coverage when in virtually cases it isn't. Make no error: If your employer is offering life insurance at no extra cost to you lot, it'south a bully benefit. By all means, get insured. But if y'all need life insurance to protect your family, employer-provided coverage may not exist sufficient.

→ Acquire more well-nigh group life insurance

How the types of life insurance stack up

| Life insurance blazon | Duration | Death benefit | Premium | Cash value |

|---|---|---|---|---|

| Term life insurance | 10 to 30 years | Fixed | Level* | No |

| Whole life insurance | Life | Fixed | Level | Yeah; guaranteed |

| Universal life insurance | Life | Adaptable | Flexible | Aye; guaranteed |

| Variable life insurance | Life | Variable | Level | Yes; not guaranteed |

| Final expense life insurance | Life | Fixed | Level | No |

| Group term life insurance | i year | Fixed | Level | No |

*Increasing and decreasing premium term life insurance policies too available.

What type of life insurance is best for you lot?

Term life insurance policies are usually the best solution for most people who need affordable life insurance for a specific period in their life. Permanent life insurance policies including whole life insurance are best for people who can pay more and want life insurance that volition never elapse.

Simplified issue and guaranteed issue life insurance are options for people who might not be able to otherwise get insured because of age or poor wellness and elderly consumers who don't want to brunt their families with burial costs.

Yous should always speak to a licensed contained broker or a financial advisor to determine the all-time insurance company and policy for you. They tin help you weigh the pros and cons of each blazon of coverage and help you purchase the right type of insurance for your needs.

Frequently asked questions

What types of life insurance are there?

The main two categories of life insurance are term life insurance (which lasts for a prepare term) and permanent life insurance (which never expires). Whole, universal, indexed universal, variable, and final expense are all types of permanent life insurance. Permanent life insurance typically comes with a cash value and has higher premiums.

Which type of life insurance policy combines insurance and investing?

The cash value component of permanent life insurance policies tin be used to save or invest. Merely because cash value policies have more expensive premiums, limited investment options, and offer relatively low rates of return, they should not exist used equally a primary savings vehicle.

What kind of life insurance should I get?

The correct life insurance policy for you depends on your fiscal situation and your dependents. Term life insurance is the best choice for most people because information technology's more affordable, but whole life insurance makes sense for people who need lifelong coverage or those looking for insurance with a cash value.

Source: https://www.policygenius.com/life-insurance/types-of-life-insurance/

0 Response to "Which Policy Provides the Most Coverage at the Lowest Cost for a Young Family?"

Post a Comment